When Friction Goes to Zero: AI Agents and the Death of Intermediation

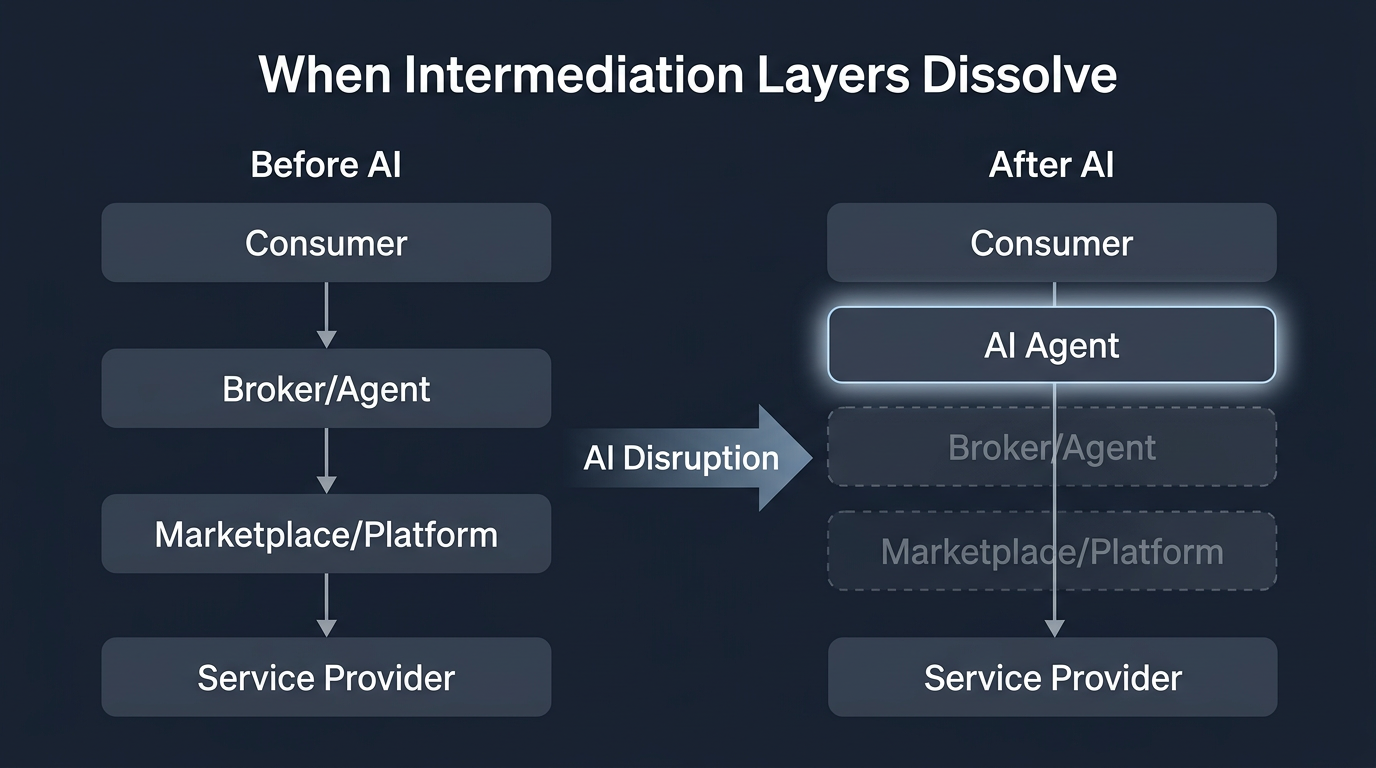

Every middleman in the economy exists because of friction. The travel agent exists because comparing 400 flights across 12 airlines is tedious. The insurance broker exists because policy documents are 90-page PDFs written in legalese. The real estate agent exists because buying a house requires navigating inspections, mortgages, and local regulations that no normal human has time to learn. AI agents don't get bored. They don't get confused by legalese. And they work for pennies per hour. This is not a technology story. It is an extinction story.

The Economics of Friction

The global economy runs on intermediation. Mastercard and Visa charge 1.5-3% interchange fees on every transaction — not because moving bits is expensive, but because they built trust infrastructure in a world where trust was hard to establish. DoorDash takes a 15-30% commission from restaurants — not because delivery logistics are inherently that expensive, but because matching demand to supply in real time used to require massive coordination overhead.

These are not evil companies extracting rent. They solved genuinely hard problems. But the problems they solved were hard for humans. An AI agent that can hold your complete travel preferences, dietary restrictions, loyalty program details, and calendar constraints in memory — and then negotiate directly with airline APIs — doesn't need Kayak or Expedia as an intermediary. It needs an API endpoint and a credit card.

"The margin is the message. Every percentage point a middleman charges is a measure of how hard the problem used to be." — Benedict Evans

Habitual Intermediation: The Real Vulnerability

Not all intermediaries are equally vulnerable. The ones at greatest risk are those that exist because of habitual intermediation — where the customer uses the middleman not because the middleman adds unique value, but because the customer has always done it that way.

Consider insurance renewal. Every year, millions of people let their car insurance auto-renew at a higher premium because comparing alternatives requires calling five companies, answering the same questions about their driving history, and parsing deductible structures. The friction cost of switching exceeds the savings for most people. An AI agent changes this calculus entirely. It can compare every insurer, negotiate rates, handle the switchover paperwork, and do it all in 90 seconds while you're brushing your teeth.

The categories most exposed to habitual intermediation:

- Travel booking: Agents, OTAs, and metasearch engines exist because comparison shopping is tedious. AI agents can negotiate directly with supplier APIs.

- Insurance: Brokers exist because policy comparison is arcane. AI agents can parse and compare policy documents at superhuman speed.

- Real estate: The 5-6% commission model has survived because transaction complexity justifies human involvement. AI agents can handle document review, scheduling, and compliance checks.

- Financial advisory: Fee-based advisors exist because portfolio management requires expertise. AI agents can now optimize tax-loss harvesting and rebalancing in real time.

- Recruitment: Staffing agencies charge 15-25% of first-year salary. AI agents can source, screen, and schedule candidates autonomously.

| Industry | Friction Type | Agent Capability | Disruption Risk |

|---|---|---|---|

| Real Estate | Information asymmetry | Property search, comp analysis | High |

| Insurance | Complexity, comparison | Policy comparison, claims | High |

| Legal | Expertise barrier | Document review, research | Medium |

| Healthcare | Navigation complexity | Symptom triage, scheduling | Medium |

| Financial Advisory | Knowledge gap | Portfolio analysis, planning | High |

The DoorDash Problem: When Platforms Become the Friction

DoorDash is instructive because it illustrates the full lifecycle. In 2018, DoorDash solved a real problem: restaurants didn't have delivery infrastructure, and consumers wanted convenience. The friction was logistical. By 2024, the friction DoorDash solved was largely operational — most restaurants could theoretically handle their own delivery, but DoorDash owned the demand aggregation.

Now consider an AI agent world. Your personal food agent knows your preferences, tracks restaurant menus, can place orders directly with restaurant ordering systems, and can coordinate delivery through a commodity logistics layer. DoorDash's 30% commission suddenly looks less like a logistics fee and more like a demand aggregation tax. And demand aggregation is precisely the kind of friction that AI agents eliminate — because the agent is the aggregator, but it works for you, not for the platform.

This is the nightmare scenario for every marketplace business: the agent disintermediates the disintermediary.

The Mastercard Parallel

Payment networks are perhaps the most entrenched intermediary in the economy. Mastercard's interchange revenue model — charging merchants 1.5-3% on every swipe — has been remarkably resilient through decades of fintech innovation. Stripe didn't displace Mastercard; it built on top of it. But AI agents create a different dynamic. If an agent can negotiate a direct ACH transfer or stablecoin payment on your behalf, the card network becomes optional rather than essential. We're not there yet — trust, fraud prevention, and regulatory compliance still justify card network fees — but the trajectory is clear.

What Survives: The Judgment Premium

Not all intermediation dies. What survives is intermediation that requires genuine judgment under uncertainty, emotional labor, or regulatory authority.

A divorce attorney doesn't just process paperwork — they navigate adversarial negotiations where the other side has a human lawyer making strategic decisions. A therapist doesn't just apply CBT protocols — they build a relationship of trust that is inherently human. A surgeon doesn't just follow a procedure — they adapt in real time to unexpected anatomy.

The pattern: if the intermediary's value is primarily information processing (comparing, sorting, matching, translating), AI agents will eat it. If the value is judgment under genuine ambiguity or human connection, it survives — for now.

The Hybrid Model

The most likely transition isn't binary. We'll see hybrid models where AI agents handle 80% of the transaction and a human specialist handles the remaining 20% that requires judgment. Real estate is a good example: an AI agent might handle property search, document review, inspection scheduling, and mortgage comparison. But the negotiation — reading the seller's motivation, deciding when to bluff, knowing when the deal is about to fall apart — might still benefit from human intuition.

The fee structure will reflect this. Instead of 6% for end-to-end service, you might pay 1% for the human-judgment slice. The AI agent's cost is negligible.

The Second-Order Effects

When friction goes to zero, the consequences extend far beyond individual industries:

- Price transparency explodes: When every consumer has an AI agent that comparison-shops every purchase in real time, price discrimination becomes nearly impossible. Airlines can't charge business travelers 4x because the agent finds the workaround.

- Brand loyalty erodes: If your agent optimizes purely on value, brand premiums compress. Why pay 20% more for the name brand when the agent confirms the generic is chemically identical?

- Service quality becomes the moat: When price and convenience are automated, the only remaining differentiator is the actual quality of the product or service. Restaurants compete on food, not on DoorDash placement.

- Employment in intermediary sectors contracts: The US has roughly 1.5 million insurance agents, 1.5 million real estate agents, and hundreds of thousands of travel agents. Not all these jobs disappear, but the ratio of agents to transactions will shift dramatically.

The Timeline Question

How fast does this happen? History suggests faster than incumbents expect but slower than technologists predict. The key bottleneck isn't technology — current AI agents are already capable enough to disintermediate many of these processes. The bottlenecks are:

- API access: Many industries (insurance, real estate) don't have open APIs. They deliberately maintain friction through proprietary systems and manual processes.

- Regulation: Licensed professions (real estate, financial advisory, legal) have regulatory barriers that slow AI adoption.

- Trust: Consumers need to trust an AI agent with their credit card, their personal data, and their decision-making. This takes time.

- Incumbent lobbying: The National Association of Realtors has 1.5 million members and significant political influence. They will not go quietly.

My estimate: within 3 years, AI agents will be the default method for insurance comparison and travel booking. Within 5 years, real estate and financial advisory will see significant commission compression. Within 10 years, the notion of paying a human 3% to process a home sale will seem as archaic as paying a human to operate an elevator.

What Should You Do?

If you're building a business that depends on intermediation:

- Audit your friction premium. What percentage of your revenue comes from information asymmetry vs. genuine value creation? The former is at risk.

- Build agent-compatible APIs. If you're a supplier (airline, insurer, restaurant), make it easy for AI agents to transact with you directly. The ones who embrace agents will get the volume.

- Move up the value chain. If you're an intermediary, shift from transaction processing to judgment and advisory. The travel agent who becomes a "luxury experience curator" survives. The one who books flights does not.

- Own the agent layer. If you can't beat disintermediation, become the agent. The company that builds the most trusted consumer AI agent captures an enormous amount of economic activity.

Commission-Based

Agents negotiate directly. Why pay 6% when an AI agent finds and negotiates better deals?

Information Arbitrage

AI democratizes access to expert knowledge. Middlemen who profit from information gaps lose their edge.

Complexity Premium

Products kept intentionally complex to justify intermediaries. AI simplifies comparison and selection.

Trust-Based (Safer)

Relationships built on genuine trust and human connection survive longest. AI augments but can't replace.

Conclusion

The economy is full of tollbooths that exist because humans are slow, forgetful, and bad at comparison shopping. AI agents are none of these things. The question isn't whether intermediation dies — it's which intermediaries can evolve fast enough to justify their existence in a world where the friction they were built to manage simply vanishes.

The best intermediaries will become advisors. The rest will become APIs.